CBS News

Mortgage interest rate forecast for summer 2024: Everything experts predict

Getty Images

Mortgage interest rates have increased so much over the last few years that it has both buyers and sellers worried. “The impact of the higher cost of homeownership has been a notable drop in home buyer demand,” says Dr. Selma Hepp, a chief economist at CoreLogic. “At the same time, higher mortgage rates have disincentivized some potential sellers to sell as they have been unwilling to give up their relatively lower rate and lower mortgage payment.”

While the demand for for-sale homes is still high, higher interest rates have slowed down the homebuying craze that occurred during the pandemic. After all, it’s not easy for potential sellers to list their homes for sale and buy something else if it means paying a higher interest rate than what they were before. And, that trend is having an impact on the market — and homebuyers.

“The combination of slower demand and low supply has reduced home sales activity to the lowest levels since the Great Financial Crisis,” Hepp says. “The typical mortgage payment has increased by over 60% since mortgage rates started increasing in mid-2022.”

But while high mortgage rates have been slowing things down, at least slightly, in recent months, what do experts think could happen this summer with mortgage rates — and, in return, the selling market? Here’s what you should know.

Find out the mortgage rates you could qualify for today.

Mortgage interest rate forecast for summer 2024: Everything experts predict

If you’re keeping an eye on this unusual mortgage rate environment, here’s what experts think could happen this summer.

Rock-bottom rates are a thing of the past

In 2021, we saw mortgage interest rates between 2% and 3% — some of the lowest rates we’ve ever had on record. Even now, mortgage rates hover around 7% for a 30-year conventional mortgage loan. While this isn’t as high as it was last October when rates climbed to almost 8%, rates are still two to three times what they were during 2020 to 2022.

Hepp doesn’t expect mortgage rates to drop that low again anytime soon.

“Three percent for a mortgage is a distant memory,” Hepp says. “It’s doubtful we will see rates that low, barring some major, adverse economic event, such as a recession, which is not expected in the near term.”

Tai Christensen, president of Arrive Home, agrees that 3% mortgage rates aren’t coming back.

“Mortgage rates could eventually drop back down to 3%,” Christensen says. “However, I doubt it will be in our lifetime, and if so, it will not be in the foreseeable future.”

Compare today’s best mortgage rates and get pre-approved for a home loan now.

Summer sizzles or summer fizzles

While spring and summer months tend to be hot for homebuying, higher interest rates could be a hindrance this summer.

“Historically, the spring and summer seasons are the most popular times to purchase homes due to favorable weather conditions and families being settled in their new property prior to the school year starting in the fall,” Christensen says. “However, since these seasons are most popular, buyers may experience increased competition and potentially higher prices.”

The average sale prices of homes sold for the first quarter of 2024 was $513,100, according to the Federal Reserve Bank of St. Louis. And, between the higher mortgage interest rates and higher home prices, there could be less incentive for people to buy.

“High mortgage rates have cooled the housing market,” Hepp says. “While it is not considered hot, there continue to be more buyers than the number of existing homes available for sale, which drives home prices higher.”

Should you buy a home now or wait?

With rates more than double what they were just a couple of years ago, many would-be homebuyers are waiting to take out mortgages right now. But that doesn’t mean you should wait, especially if you’re prepared with the funds, credit score and ideal location for buying a home.

“Mortgage rates are expected to start moving lower by the end of this year,” Hepp says. “However, this is largely dependent on overall inflation and whether the Fed gains confidence in the [persistence] of disinflation. In that case, the Fed would lower the federal funds rate, which would help bring mortgage rates lower as well.”

Buying now might be the right choice if:

- You have a large chunk in a down payment. If it’s 20% or more, you can avoid paying private mortgage insurance.

- You have excellent credit and have shopped around with lenders to get the lowest interest rate available.

- You plan on staying in your home for a while.

- You’re willing to consider a 15-year mortgage, which tends to have lower interest rates than 30-year loans.

- You plan on refinancing your home when rates drop to take advantage of the dip.

The bottom line

Ultimately, buying now isn’t required and for some potential buyers, now isn’t the right time. If you can hold off for a while, you may be able to get a lower mortgage rate and have less competition — but it all depends on what happens with the economic conditions in the future.

“Purchasing during less popular times, like fall or winter, could increase a buyer’s ability to negotiate more favorable terms,” Christensen says.

If you choose to buy now, though, there may be benefits to doing so. And, you aren’t stuck with today’s high mortgage rates forever. You have the option to refinance in the future if rates decline, so if you find the perfect home and are able to make your move now, it may be worth snagging your dream home instead of missing out.

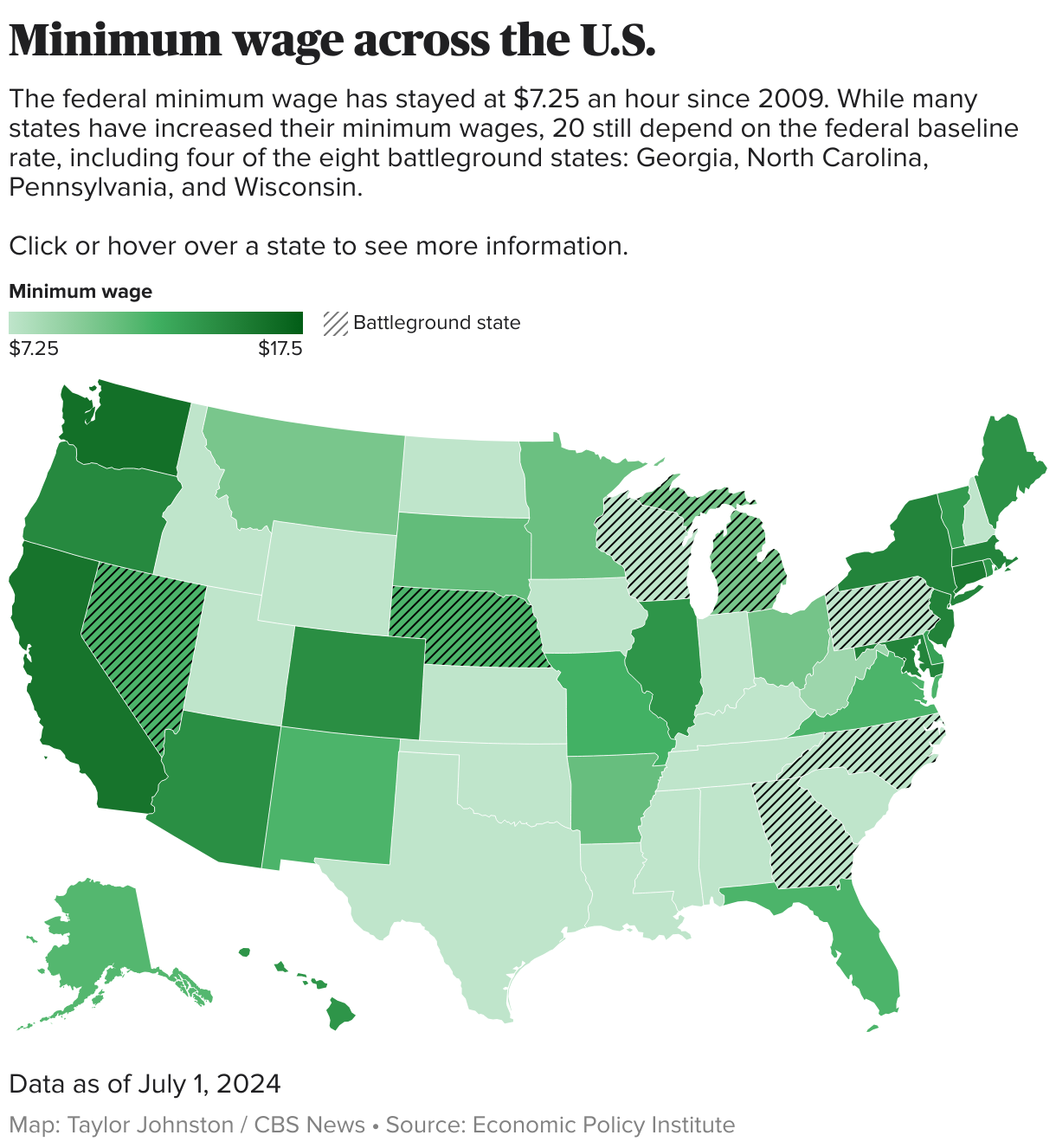

Half of the eight battleground states in this year’s U.S. presidential election use the federal minimum wage of $7.25 an hour, a rate that hasn’t changed since 2009 despite a 47% surge in the cost of living since then. In essence, that means minimum-wage workers in those states have seen much of their purchasing power vaporized by inflation over the past 15 years.

Donald Trump’s October 20 visit to a McDonald’s location in Feasterville, Pennsylvania, where the former president served food to pre-selected supporters, has renewed public attention on how much low-income workers earn. Asked by CBS News reporter Olivia Rinaldi if he thought the minimum wage should be raised after spending time behind the counter at the fast-food restaurant, Trump sidestepped the question.

“Well, I think this. I think these people work hard. They’re great,” he said. “And I just saw something a process. It’s beautiful. It’s a beautiful thing to see. These are great franchises and produce a lot of jobs, and it’s good and great people working here too.”

Trump’s campaign didn’t immediately respond to a request for comment about the former president’s views on the minimum wage.

Vice President Kamala Harris has stated that she wants to raise the nation’s minimum wage, as well as the sub-minimum wage that is earned by tipped workers. Both Trump and Harris have proposed eliminating income taxes on tips as a way to boost earnings for people in the hospitality industry.

While the federal minimum wage has been frozen since 2009, 30 states have stepped in to boost wages for their lowest-earning workers, according to the left-leaning Economic Policy Institute. That’s left 20 states still paying the federal baseline wage, representing annual earnings of $15,000. Those states are mostly in the South and Midwest, including the four battleground states that use the $7.25 an hour minimum: Georgia, North Carolina, Pennsylvania and Wisconsin.

Experts note tha workers in these locations are at risk of falling behind people who reside in states providing a higher pay floor.

“It’s ridiculous that Pennsylvania has a lower minimum wage than its neighbors as well as states like Arkansas, Florida and Nebraska, where voters had a chance to pass raises through ballot initiatives,” Holly Sklar, CEO of Business for a Fair Minimum Wage, a group that advocates for higher pay, told CBS MoneyWatch.

Earning $7.25 an hour “is a poverty wage, and it’s bad for business as well as workers,” Sklar added.

The minimum wage versus inflation

The renewed focus on worker pay comes amid polling that shows many people continuing to struggle financially even as inflation fades and the job market continues to click.

A majority of Americans say they feel worse off than four years ago, according to Gallup, a pessimism that could sway their decisions in the November 5 election. And 6 in 10 voters describe the U.S. economy as either “fairly bad” or “very bad,” according to CBS News polling.

That is likely tied to elevated prices caused by the hottest inflation in 40 years, which outpaced wage growth during the pandemic. Yet since May 2023, the typical worker’s pay has outpaced inflation, boosting their purchasing power.

That isn’t the case for workers who earn the federal minimum wage because it isn’t indexed to inflation, a step that some states are now taking to ensure that people can keep up with the rising cost of living. If the federal minimum wage had been indexed for inflation, it would now stand at $10.61 per hour.

The four other battleground states have lifted their hourly minimum wage to about that level, or even higher:

- Arizona: $14.35 an hour

- Michigan: $10.33 an hour

- Nebraska: $12 an hour

- Nevada: $12 an hour

“In our region, the minimum wage has gone up in surrounding states but not in Pennsylvania,” noted Keystone Research Center, a think tank for Pennsylvania-related issues, in a blog post. “Minimum-wage workers in Pennsylvania have also lost ground relative to workers in the middle of the wage distribution, that is, relative to the median wage.”

Tom Zawierucha, 58, a building services worker in New Jersey, wishes candidates would talk more about protecting older Americans from big medical bills.

Teresa Morton, 43, a freight dispatcher in Memphis, Tennessee, with two teenagers, wants to hear more about how elected officials would help working Americans saddled with unaffordable deductibles.

Yessica Gray, 28, a customer support representative in Wisconsin, craves relief from high drug prices and medical bills that have driven her and her husband deep into debt. “How much are we going to pay?” she said. “It’s just something that’s always on my mind.”

Health care hasn’t figured prominently in this increasingly acrimonious presidential campaign. And the economy has generally topped the list of voters’ concerns.

But Americans remain intensely worried about paying for medical care, national surveys show.

Two in 3 U.S. adults in a recent nationwide poll by West Health and Gallup said they’re concerned a major health event would land them in debt. A similar share said health care isn’t getting enough attention in the campaign.

To better understand voters’ health care concerns as the 2024 campaign nears an end, KFF Health News worked with research firm PerryUndem to convene a pair of focus groups last week with 16 people from across the country. PerryUndem is a nonpartisan firm based in Washington, D.C., that studies public views on health care and other issues.

The focus group participants represented a broad swath of the electorate, with some favoring Republican candidates, and others Democrats. But nearly all shared a common complaint: Neither presidential candidate has talked enough about how they’d help people struggling to pay for medical care.

“You don’t really hear anything much about health care costs,” said Bob Groegler, 46, who works in residential financing in eastern Pennsylvania. Groegler said he’s worried he may never be able to retire because he won’t have enough money to pay his medical bills.

Former President Donald Trump, the Republican nominee, hasn’t offered a detailed health care agenda, though he criticizes current laws and said he has “concepts of a plan” to improve the 2010 Affordable Care Act, often called Obamacare.

Vice President Kamala Harris, a Democrat, has laid out more detailed health care proposals, including building on legislation signed by President Joe Biden to lower patients’ bills.

In 2022, Biden signed the Inflation Reduction Act, which limits how much Medicare enrollees must pay out-of-pocket for prescription drugs, including a $35 monthly cap on insulin. The legislation also provides additional federal aid to help Americans buy health insurance through the Affordable Care Act, though this aid will expire unless Congress and the president renew it next year.

Harris has said she will expand the aid and push for new assistance to Medicare enrollees who need home care. She also has pledged to continue federal efforts to relieve medical debt, a nationwide problem that burdens about 100 million people.

But most of the focus group participants said they knew little about these proposals, complaining that hot-button issues like abortion have dominated the campaign.

Many also expressed deep skepticism that either Harris or Trump would do much to lighten the burden of medical bills.

“I believe they’re out of touch with our reality,” said Renata Bobakova, 46, a teacher and mother outside Cleveland. “We never know when we’ll get sick. We never know when we’ll fall down or sprain an ankle. And prices really can be astronomical. … I’m constantly worried about that.”

Bobakova, who is from Slovakia, said she went back to Europe to give birth to her daughter 10 years ago to avoid crippling medical debt she knew she’d incur in this country. Parents with private health coverage face on average more than $3,000 in medical bills related to a pregnancy and childbirth that aren’t covered by insurance.

Other focus group participants said they or people they knew had left the country to get cheaper prescription drugs. The U.S. has the highest medical prices in the world, research shows.

Several focus group participants, such as Kevin Gaudette, 64, a retired semiconductor engineer in North Carolina, blamed large hospitals, drug companies, and insurers for blocking efforts to lower patients’ costs to protect their profits. “I think everybody has their finger in the pie,” Gaudette said.

Martha Chapman, 64, who is also retired and lives in Philadelphia, pointed to what she called “corporate greed.” “I just don’t think it’s going to change,” she said.

In the closing days of the campaign, that cynicism represents a particular problem for Harris, said PerryUndem co-founder Michael Perry, who led the two focus groups.

Harris has tried to distinguish herself as the candidate who is more serious about policy and more sympathetic to voters’ economic struggles, Perry said. And in recent weeks, she’s begun airing new ads highlighting health care issues.

But even focus group participants who said they lean Democratic seemed to blame both candidates for not addressing Americans’ health care concerns. “They’re not feeling listened to,” Perry said.

Many of the participants nevertheless continued to express hope that an issue as important as health care would someday get the attention of elected officials, regardless of political party.

“We’re all human beings here. We’re all people just trying to make it,” said Zawierucha, the building services worker in New Jersey. “If we get sick or have to go in and get something done, we should have that peace of mind that we can go in there and not have to worry about paying it off for the next 20 years.”

“Just give us some peace of mind,” he said.

KFF Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at KFF — the independent source for health policy research, polling and journalism.

Cardi B says she’s been hospitalized with a medical emergency and will have to miss a Saturday night headlining performance at an Atlanta music festival.

“I am so sad to share this news, but I’ve been in the hospital recovering from a medical emergency the last couple of days and I won’t be able to perform at ONE MusicFest,” the Grammy-winning rapper wrote on Instagram. “It breaks my heart that I wont get to see my fans this weekend.”

She added, “I’ll be back better and stronger soon. Don’t Worry.”

Johanna Geron / REUTERS

The 32-year-old New York native gave no details on her condition.

Cardi gave birth to her third child with rapper Offset less than two months ago. The two are going through a divorce.

She was to have performed along with Earth, Wind & Fire, Nelly, Gunna and GloRilla at the two-day ONE Musicfest.