CBS News

Will credit card debt forgiveness cover my $25,000 debt?

Getty Images

Inflation fell in September after hitting a 3-year low in August. Unemployment numbers are low and the Federal Reserve just issued its first interest rate cut in more than four years. While these are all encouraging signs for the broader economy, it will take some time for consumers to recover from recent financial troubles. It wasn’t that long ago that inflation was at a decades-high and interest rates are still exponentially higher than they were just a few years ago.

Against this backdrop, credit card debt has surged with the average user now owing approximately $8,000 to their lenders. And with the average credit card interest rate hovering near a record 23%, it will take a long time and a concentrated effort to reduce that balance. For many borrowers, it may make sense to pursue debt relief, specifically credit card debt forgiveness. However, there are some limits to what this service can do for borrowers. So, will credit card debt forgiveness cover a $25,000 debt?

See how debt relief can help reduce what you owe here now.

Will credit card debt forgiveness cover my $25,000 debt?

In short: yes, a credit card debt forgiveness program can cover your $25,000 debt. The minimum balance for this type of service is typically $7,500. But that doesn’t mean you’ll get your entire balance wiped clean. Credit card debt forgiveness programs typically cover 30% to 50% of the existing balance. So, in this circumstance, you may be able to settle for between $7,500 and $12,500. But you’ll need to qualify for that relief. Specifically, most companies will want you to provide all of the following:

- Debt over $7,500: This applies in this circumstance but if you owe less than that amount you may be better served by turning to a debt relief alternative.

- Financial hardship: If you can demonstrate you’re currently experiencing a financial hardship that’s preventing you from paying your balance, you can improve your chances of approval. This means showing the loss of a job, medical expenses, or more. You’ll need to provide documentation demonstrating this hardship.

- Behind on payments: You’re more likely to get help with forgiving a balance if you’re already behind on your monthly payments. If you’ve been staying up to date, even if with minimal payments, creditors are less likely to help, since that typically demonstrates an ability to make payments, just at a slower pace.

If you currently qualify for forgiveness then consider contacting a servicer now. With credit card rates high and predicted rate cuts unlikely to make a material difference in what you owe, it makes sense to be proactive.

Start tackling your high-rate credit card debt now.

What about a debt consolidation loan?

Credit card interest rates are high now but personal loans are much lower (averaging just under 13% compared to credit card rates at 23%). It can be beneficial for many borrowers to then consolidate their existing credit card debt with a lower-rate consolidation loan. Rates will depend on your credit score and profile but, if your score is high, you will likely qualify for a low-rate loan. This won’t eliminate a portion of your debt like a forgiveness plan would, but you also won’t have to deal with the credit score ramifications that most forgiveness plans result in, either.

The bottom line

If you meet certain criteria, a credit card debt forgiveness program can cover a $25,000 balance. But it won’t cover it in its entirety. And, in many cases, borrowers may be better served by exploring alternatives like debt consolidation loans. No matter which option you ultimately choose, however, don’t let your debt stagnate, particularly at today’s elevated. Explore all of your best debt relief options and choose the one that works best for your financial situation right now.

CBS News

Shrinkflation has affected one-third of grocery items, analysis finds. Here are the worst offenders.

Americans continue to face higher prices after inflation shot up during the pandemic, in particular for essentials like food. But there’s another, less noticeable, trend that’s just as painful to your pocketbook eve when a product’s cost looks stable: shrinkflation.

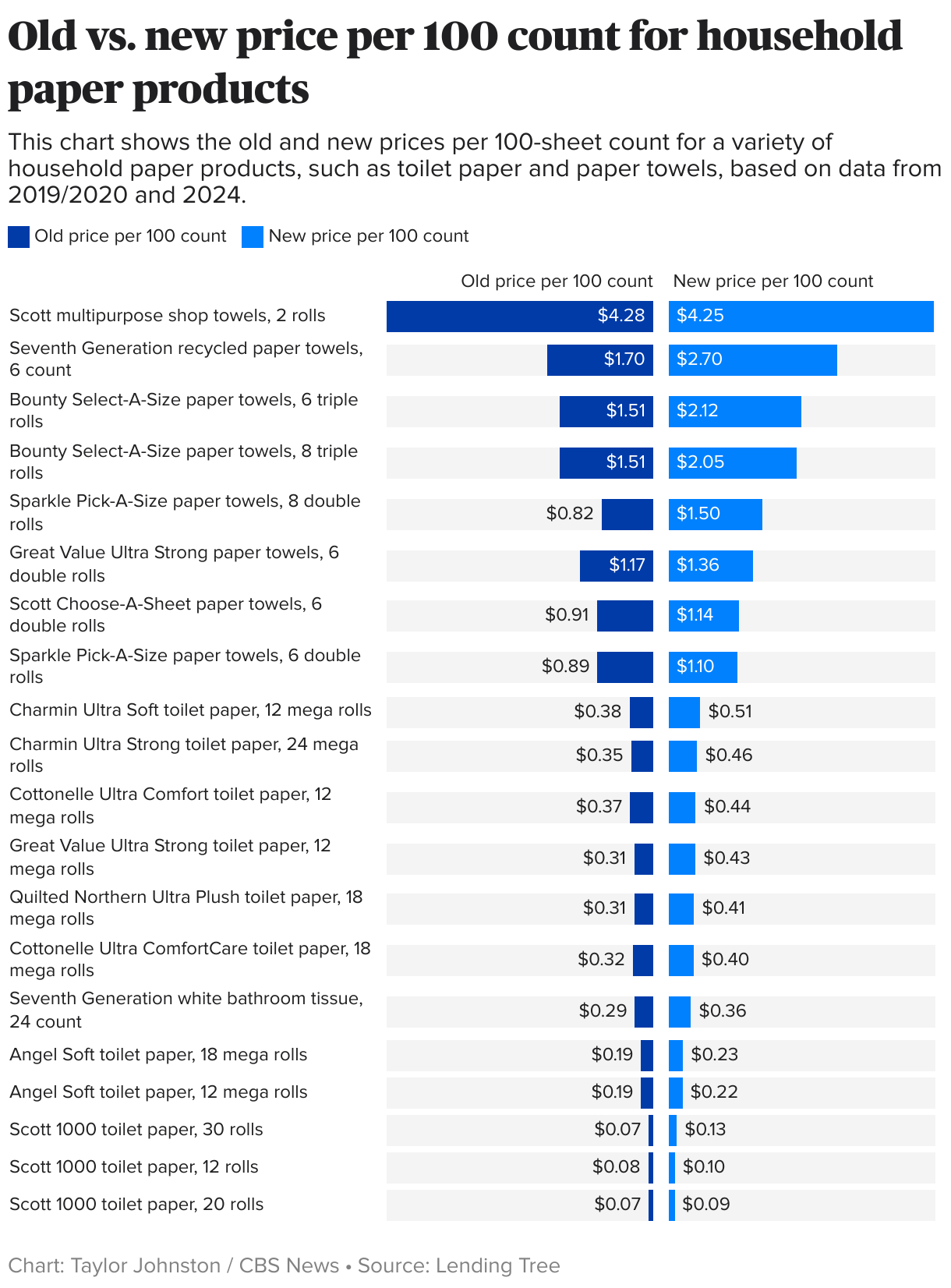

About one-third of roughly 100 common consumer products tracked by LendingTree have shrunk in size or servings since the pandemic. The worst offenders — household paper products, like toilet paper and paper towels, personal finance firm’s analysis found.

More specifically, shrinkflation refers to scaling back the size of a product but charging the same amount as for the prior, larger portion. The upshot: People end up shelling out more money because they’re getting less of a given product.

To be sure, shrinkflation is by no means a new consumer phenomenon. The term is credited to British economist Pippa Malmgren in 2009, but the trend picked up in the post-pandemic years as corporations wrestled with higher manufacturing costs. Instead of hiking prices and potentially losing shoppers, some opted to make their products smaller while continuing to charge the same amount.

Inflation in August hit a three-year low. That doesn’t necessarily mean prices are falling; rather, the pace of price increases has slowed sharply compared to the outsized spikes experienced during pandemic, when inflation hit a 40-year high. But with shrinkflation remaining an issue with many products, about 7 in 10 consumers said they’ve noticed at least one incident of the trend within the last year, according to LendingTree.

“The fact we were able to find one-third of these products having shrunk, and in some categories an even bigger percentage, it’s a troubling thing,” LendingTree chief credit analyst Matt Schulz told CBS MoneyWatch. “Nobody loves high prices, but people would prefer to pay a little bit more if the alternative is paying the same and getting less, and not really being told about it.”

Shrinkflation can often be tough to document or even pick up on, given that many people don’t keep older packages of, say, toilet paper or cereal on hand with which to compare newer purchases, Schulz noted. LendingTree tracked the issue by comparing Walmart’s prices in 2024 with those in 2019-2020 via the Wayback Machine, a site that archives webpages from prior months and years.

Still, many consumers aren’t fooled, and the trend has drawn condemnation from everyone from Cookie Monster, who declared on X in August that “me hate shrinkflation!” because it was making his cookies smaller, to President Joe Biden, who called on snack companies in February to stop the shrinkage.

A similar trend is “skimpflation,” where the quality of a product or service is reduced to save money, such as switching to a cheaper ingredient or cutting back on services at a hotel or restaurant.

Products with the most shrinkflation

Household paper products have the highest rate of shrinkflation, the LendingTree analysis found. Out of 20 products it tracked from prior to the pandemic until today, about 60% had reduced their sheet count, the study found.

Breakfast foods had the second-highest rate of shrinkflation, with LendingTree finding that about 44% of the items they tracked were now sold in smaller portions. Family-sized Frosted Flakes, made by Kellogg’s, has slimmed from 24 ounces to 21.7 ounces, resulting in a 40% increase in per-ounce pricing, the analysis found.

About 38% of candy items are now sold in smaller amounts, including party-size Reese’s miniatures (35.6 ounces now versus 40 ounces in 2019-2020) and party-size milk chocolate M&M’s (38 ounces now versus 42 ounces previously.)

About 27% of snacks had gone through portion reductions, LendingTree said. That includes party-size Cheetos, made by Frito-Lay, which shrank to 15 ounces from 17.5 ounces while its per-ounce price rose to 40 cents from 17 cents.

Other snacks that have gotten smaller but pricier include party-size sour cream and onion Lay’s, family-size original Wheat Thins and party-size original Tostitos, LendingTree said.

Shrinkflation’s impact on your finances

Shrinkflation can make household budgeting even tougher for consumers because it’s harder to prepare for, Schulz noted.

“In general the average American’s financial margin for error is super tiny, and this is just another thing that makes that situation a little bit harder,” he said.

Items that are rising in price due to inflation may be easier to budget simply because shoppers can clearly see the higher prices and account for it in their spending, Schulz added.

“But if the thing you’re buying stays the same price, but has less, it’s not as readily noticeable and it may create a distortion in your budget,” he said.

Watch CBS News

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.

Watch CBS News

Be the first to know

Get browser notifications for breaking news, live events, and exclusive reporting.